Baillie Gifford

Emerging Market investing – Why do we do what we do?

By Andrew Kellier, Client Service Director at Baillie Gifford

Our investment philosophy hasn’t changed since we started running dedicated emerging markets (EM) portfolios in 1994. We’ve always been active, focused on growth and never allowed ourselves to get bogged down in short-term earnings estimates or price targets. Here, we answer: why do we invest in EM equities in the way that we do?

We would strongly suggest that EM equity is an asset class where active management works best and where having a dedicated EM manager makes sense.

This is backed up in a study by Copley’s Fund Research1, which shows that active EM has outperformed passive on periodic returns over 10 years and 20 years after fees. But unfortunately, it’s not as simple as pick an active EM manager and you will outperform. There is a huge spread in active management performance, with more than a 100 per cent difference in cumulative return over a 10-year period between the best performers and the worst performers. It is the select few top performers that skew the active management average to the upside. Manager selection matters.

We warn against holding the index not just because passive investing forces investors to hold big companies which probably won’t exist in 20 years, or because the EM index contains several state-controlled companies (SOEs) that do not have the dynamism that EM stocks are supposed to provide. It’s simply because most ‘emerging markets’ don’t emerge. For example, in the last 15 years, the Greek stock market has fallen by almost 20 per cent per annum (pa).

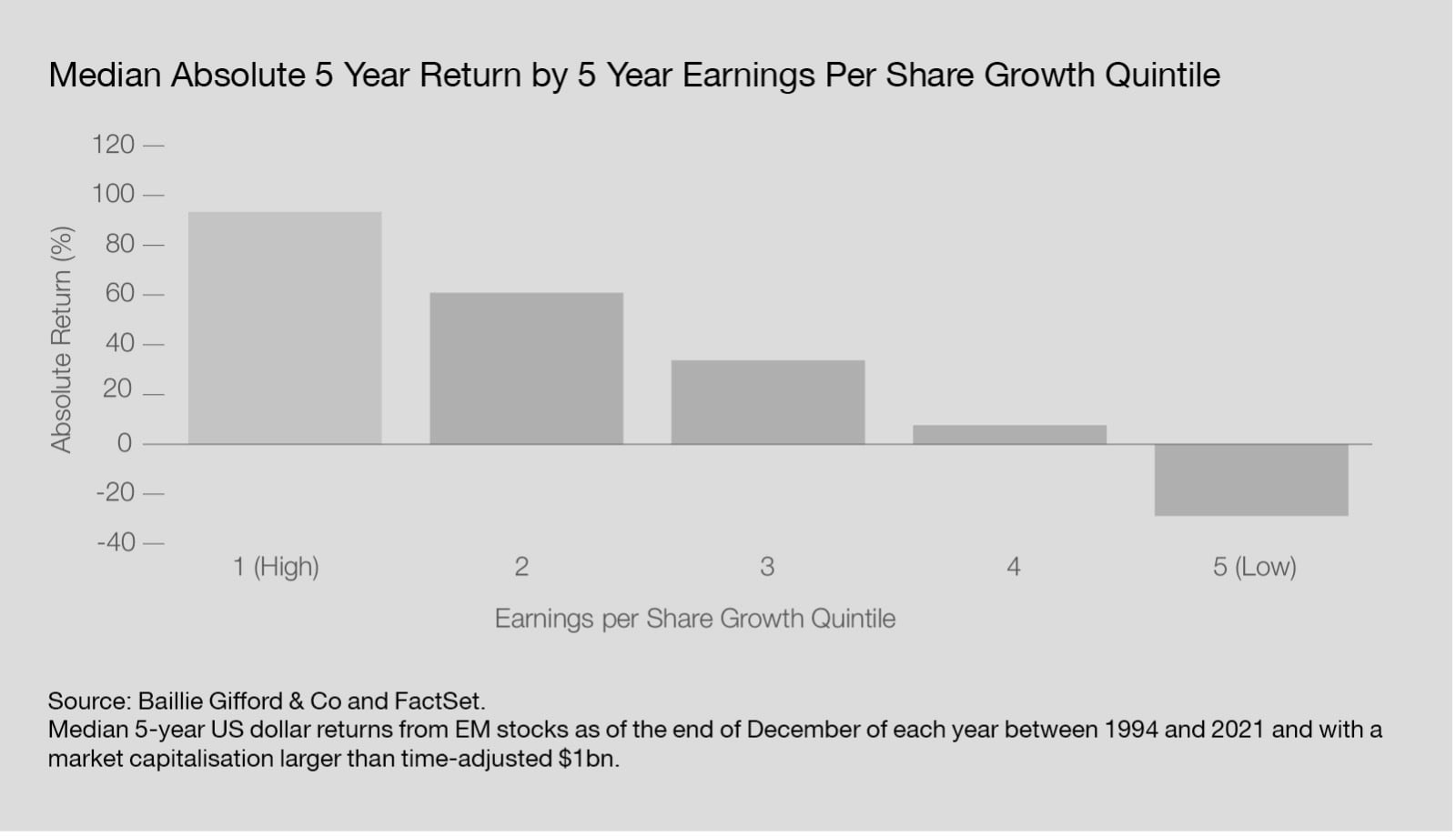

Underpinning our commitment to growth investing is the belief that, ultimately, those companies which can sustainably grow their earnings will be rewarded by the market. To evidence this we looked at different quintiles of earnings growth, in US dollars, over five-year periods in the EM universe. Since 1994, the best quintile of earnings growers in each five-year period were rewarded, on a median basis, with a near doubling in share price in US dollars over that five-year period.

By definition, investing in EM means you are gaining exposure to the world’s fastest growth economies. But in truth, gross domestic product (GDP) growth doesn’t always lead to high stock market returns.

By definition, investing in EM means you are gaining exposure to the world’s fastest growth economies. But in truth, gross domestic product (GDP) growth doesn’t always lead to high stock market returns. Several studies have examined this in detail. They confirm you can’t hope that simply investing in a bunch of high-growth economies will make you above-average returns in hard currency terms. Take Türkiye, for example, which has grown its GDP at an admirable 4.8 per cent pa in US dollar terms over the last 15 years and yet its stock market has contracted by 3.7 per cent pa. We took a look at ‘big winners’ in EM, defining those as companies which have delivered 20 per cent pa total return in US dollar terms over a ten-year horizon, ie more than a six-fold return. We found that these highly successful companies were subject to rocky price trajectories, suffering an average maximum drawdown of 63 per cent during the ten-year window. Clearly, this is significant and gives some indication of the tolerance required of investors to access these substantial returns over the long term. Short-term discomfort comes with the territory.

We set a high bar for investment; we need to be able to envisage a scenario where the company can at least double in hard currency terms over five years. So, the next question is, do we manage to find these big winners? It’s unrealistic to expect every company we invest in to provide such strong returns, but it is hopefully informative that over 50 per cent of all stocks held in the Baillie Gifford Emerging Markets All Cap Fund for five years or more have delivered this doubling (more than 30 per cent have tripled and 15 per cent have quintupled). However, this is not simply a ‘buy and hold’ strategy, we regularly review portfolio holdings to ensure that the upside case is intact.

We believe that the chance of strong absolute returns from EM is significant on a long-term view. This is about a lot more than just high GDP growth, favourable demographics and rising middle-class incomes. Many companies are displacing established peers and dominating relatively new industries, while still growing at a rate well in excess of the broader market. EM investors are being given the opportunity to invest in companies that we believe will dominate in years to come, not just in their home markets but globally, and in the process, generate world-class returns.

Our clients can be confident that we will still be working to the same principles in the future that we do today. We will continue to invest in EM, we will be active, and we will be seeking to identify substantial growth opportunities with the confidence our clients will be rewarded over the long term.

1Copley Fund Research specialise in Global, GEM and Asia Ex-Japan fund positioning, fund flows and fund performance.

The value of your investment and any income from it can go down as well as up and as a result your capital may be at risk. This article does not constitute, and is not subject to the protection afforded to, independent research. Baillie Gifford and its staff may have dealt in the investments concerned. The views expressed are not statements of fact and should not be considered as advice or a recommendation to buy, sell or hold a particular investment. Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA).