Neuberger Berman

Copper May Soon Be In Short Supply

By Hakan Kaya, Senior Portfolio Manager at Neuberger Berman

Copper appears a cornerstone of the green-technology revolution. With global supply constrained, we think prices could soon be on the rise.

Hakan Kaya, Senior Portfolio Manager, will be discussing in the Alternatives Breakout Session how copper, a linchpin of the green energy revolution, appears to face a looming supply-demand imbalance that, in our view, could soon shine up the metal’s market price.

On the demand side, government initiatives—such as the U.S. Inflation Reduction Act, RePower Europe, and “net-zero” commitments around the globe—are turbocharging the need for copper, which is a crucial component in everything from electric vehicles to solar photovoltaic plants. As the transition to clean energy accelerates, we expect copper demand to grow exponentially, helped along by the global “green space race.” For example, when China offered subsidies for building battery plants (a strategically important initiative), the U.S. and EU followed suit. We think that sort of global one-upmanship could drive even further demand in years to come.

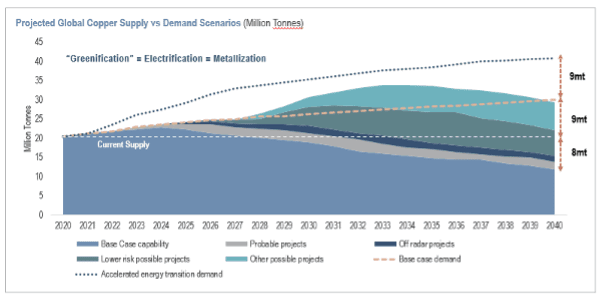

Figure 1: The Green Revolution’s Demand For Copper Could Soon Outstrip Supply

As for supply, yields from gradually exhausted mines have been declining for decades, while new-mine construction confronts long-cycle risks (it takes 10-12 years to open a new mine), and general underinvestment due to historically poor returns. Copper supplies are also geologically concentrated across a few countries, potentially restricting supply. Essentially, copper could become “the new oil”.

Source: Wood Mackenzie. Data as at 23 March 2021.

Figure 1 tells the tale. During calendar year 2020, the world produced 20 million metric tons of copper. At that “base case capability” (meaning no new mines are built), production is expected to fall roughly 8 million metric tons by 2040 as existing mines gradually exhaust; meanwhile, baseline demand is expected to climb by 9 million tons.

That supply-demand mismatch could widen further along the way, depending on the price of copper and the trajectory of the global green-energy transition (see the dotted “accelerated energy transition demand” line on figure 1). While higher prices could incentivize new mine development, the shift toward electric vehicles, renewable power and other clean technologies could propel annual copper demand even further.

Recycling may provide some supply relief—however, it is a very expensive process and we believe copper prices would need to rise to compensate for the effort. Substitution doesn’t appear a viable option, either: Unlike other metals, copper boasts a unique combination of ductility and conductivity, making it ideal for a host of applications, including batteries, wiring, electrical grids and more.

All factors considered, by how much might copper prices rise?

For historical context, consider China’s rapid development during the early 2000s. During that period, rising prices for energy commodities and industrial metals sent the Bloomberg Commodity Industrial Metals subindex soaring more than 400% until the Great Financial Crisis arrived in 2008. In our view, total capital outlays to support the green revolution could exceed twice China’s demand for metals during its heyday—making a good case, in our view, that the Metals subindex could surpass its huge runup during the aughts.

In even more tangible terms, consider that the Escondida mine in northern Chile—the largest copper mine in the world—produces around 1 million tons of copper per year. To meet demand implied by current 2050 global net-zero goals, we estimate the world will need one new Escondida mine every year through 2030.

In our view, commodity investors might be wise to buy what’s in short supply. The value of a commodity is directly related to its scarcity rather than its production. An active approach allows investors to benefit from this counterintuitive risk dynamic, while passive investments follow production weightings and could lead to risk concentration.

Neuberger Berman Commodities Fund

We believe global structural shifts like the transition to carbon neutrality support the long-term strategic positioning in commodities. As we complete this transition, many commodities will become scarcer and become more valuable, making the case for a broader allocation. We invest with a fully diversified broad-based approach to capitalise on the breadth of opportunities.

Neuberger Berman has managed diversified commodities since May 2010 using a scarcity and risk-aware approach that seeks to encompass both current and future scarcity at a reasonable risk. The team has established an attractive track record with their rigorous process and high-quality research. The Neuberger Berman Commodities Fund was launched in 2022 and could be suited to investors looking to tap into global growth trends and hedge against inflation or diversify risk. The investment team utilise unique data sources and analytics for enhanced insights, seeking to provide an attractive level of return investing across various commodity sectors via commodity-related derivative instruments.

Find out more about the fund

Key risks

Market Risk: The risk of a change in the value of a position as a result of underlying market factors, including among other things, the overall performance of companies and the market perception of the global economy.

Liquidity Risk: The risk that the portfolio may be unable to sell an investment readily at its fair market value.

Counterparty Risk: The risk that a counterparty will not fulfil its payment obligation for a trade, contract or other transaction, on the due date.

Interest Rate Risk: The risk of interest rate movements affecting the value of fixed-rate bonds.

Credit Risk: The risk that bond issuers may fail to meet their interest repayments, or repay debt, resulting in temporary or permanent losses to the portfolio.

Derivatives Risk: The fund may use certain types of financial derivative instruments (including certain complex instruments). This may increase the portfolio’s leverage significantly which may cause large variations in the value of investments. Investors should note that the fund may achieve its investment objective by investing principally in Financial Derivative Instruments (FDI). There are certain investment risks that apply in relation to the use of FDI.

Operational Risk: The risk of direct or indirect loss resulting from inadequate or failed processes, people and systems including those relating to the safekeeping of assets or from external events.

Currency Risk: Investments in a currency other than the base currency of the portfolio are exposed to currency risk. Fluctuations in exchange rates may affect the return on investment. If the currency of the portfolio is different from your local currency, then you should be aware that due to exchange rate fluctuations the performance may increase or decrease if converted into your local currency.

Model Risk: The investment strategy of a portfolio using a quantitative investment approach is rules based and model-driven. Therefore, it would not necessarily result in a security being sold because that security’s issuer was in financial trouble or defaulted, or had its credit rating downgraded, unless such indicators are tracked by the investment strategy of that portfolio. There is no guarantee that the investment strategy of such a portfolio will meet the purpose for which it was designed.

Commodity Risk: The Fund's exposure to the commodities markets, and/or a particular sector of the commodities markets, may subject the Fund to greater volatility than investments in traditional securities, such as stocks and bonds. The commodities markets are impacted by a variety of factors, including changes in overall market movements, resource availability, commodity price volatility, political and economic events and policies, interest rates and inflation rates.

For full information on the risks please refer to the fund prospectus and KIID.

Disclaimer

This document is addressed to professional clients/qualified investors only.

United Kingdom and outside the EEA: This document is a financial promotion and is issued by Neuberger Berman Europe Limited, which is authorised and regulated by the Financial Conduct Authority and is registered in England and Wales, at The Zig Zag Building, 70 Victoria Street, London, SW1E 6SQ.

Neuberger Berman Europe Limited is also a registered investment adviser with the Securities and Exchange Commission in the US, and the Dubai branch is regulated by the Dubai Financial Services Authority in the Dubai International Financial Centre.

This fund is a sub-fund of Neuberger Berman Investment Funds PLC, authorised by the Central Bank of Ireland pursuant to the European Communities (Undertaking for Collective Investment in Transferable Securities) Regulations 2011, as amended. The information in this document does not constitute investment advice or an investment recommendation and is only a brief summary of certain key aspects of the fund. Investors should read the prospectus along with the relevant prospectus supplements and the key information document (KID) or key investor information document (KIID), as applicable which are available on our website: https://link.edgepilot.com/s/be4a4d48/FAnf0T427k2XxUNrGdCdgw?u=http://www.nb.com/europe/literature. Further risk information, investment objectives, fees and expenses and other important information about the fund can be found in the prospectus and prospectus supplements.

The KID may be obtained free of charge in Danish, Dutch, English, Finnish, French, German, Greek, Icelandic, Italian, Norwegian, Portuguese, Spanish and Swedish (depending on where the relevant sub-fund has been registered for marketing), and the prospectus and prospectus supplements may be obtained free of charge in English, French, German, Italian and Spanish, from https://link.edgepilot.com/s/be4a4d48/FAnf0T427k2XxUNrGdCdgw?u=http://www.nb.com/europe/literature, from local paying agents (a list of which can be found in Annex III of the prospectus), or by writing to Neuberger Berman Investment Funds plc, c/o Brown Brothers Harriman Fund Administration Service (Ireland) Ltd, 30 Herbert Street, Dublin 2, Ireland. In the United Kingdom the key investor information document (KIID) may be obtained free of charge in English at the same address or from Neuberger Berman Europe Limited at their registered address.

Neuberger Berman Asset Management Ireland Limited may decide to terminate the arrangements made for the marketing of its funds in all or a particular country.

A summary of the investors’ rights is available in English on: https://link.edgepilot.com/s/be4a4d48/FAnf0T427k2XxUNrGdCdgw?u=http://www.nb.com/europe/literature

For information on sustainability-related aspects pursuant to Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on sustainability‐related disclosures in the financial services sector please visit https://link.edgepilot.com/s/be4a4d48/FAnf0T427k2XxUNrGdCdgw?u=http://www.nb.com/europe/literature. When making the decision to invest in the fund, investors should take into account all the characteristics or objectives of the fund as described in the legal documents.

This document is presented solely for information purposes and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security.

We do not represent that this information, including any third-party information, is complete and it should not be relied upon as such.

No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of any investment, and should consult its own legal counsel and financial, actuarial, accounting, regulatory and tax advisers to evaluate any such investment.

It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. Investors may not get back the full amount invested.

Any views or opinions expressed may not reflect those of the firm as a whole.

All information is current as of the date of this material and is subject to change without notice.

The fund described in this document may only be offered for sale or sold in jurisdictions in which or to persons to which such an offer or sale is permitted. The fund can only be promoted if such promotion is made in compliance with the applicable jurisdictional rules and regulations. This document and the information contained therein may not be distributed in the US.

Indices are unmanaged and not available for direct investment.

An investment in the fund involves risks, with the potential for above average risk, and is only suitable for people who are in a position to take such risks. For more information please read the prospectus which can be found on our website at: https://link.edgepilot.com/s/be4a4d48/FAnf0T427k2XxUNrGdCdgw?u=http://www.nb.com/europe/literature.

Past performance is not a reliable indicator of current or future results. The value of investments may go down as well as up and investors may not get back any of the amount invested. The performance data does not take account of the commissions and costs incurred by investors when subscribing for or redeeming shares.

The value of investments designated in another currency may rise and fall due to exchange rate fluctuations in respect of the relevant currencies. Adverse movements in currency exchange rates can result in a decrease in return and a loss of capital.

Tax treatment depends on the individual circumstances of each investor and may be subject to change, investors are therefore recommended to seek independent tax advice.

Investment in the fund should not constitute a substantial proportion of an investor’s portfolio and may not be appropriate for all investors. Diversification and asset class allocation do not guarantee profit or protect against loss.

No part of this document may be reproduced in any manner without prior written permission of Neuberger Berman.

The “Neuberger Berman” name and logo are registered service marks of Neuberger Berman Group LLC.

© 2023 Neuberger Berman Group LLC. All rights reserved.