Schroders

The good, the bad and the ugly

By Julien Houdain, Head of Credit at Schroders

There are many situations that could influence corporate bond investment performance in the next 12 months. Making a single prediction about where corporate debt markets are going is fraught with difficulty. The best way to look at this is to consider how corporate bonds might behave under three different scenarios. From this, we can then look at the implications for investors.

Three possible scenarios: Let’s start with the economic backdrop and set up three possible combinations of inflation, interest rates and growth which we’ll call The Good, The Bad and the Ugly. Amazingly, the market priced in all three scenarios during the first few months of 2023.

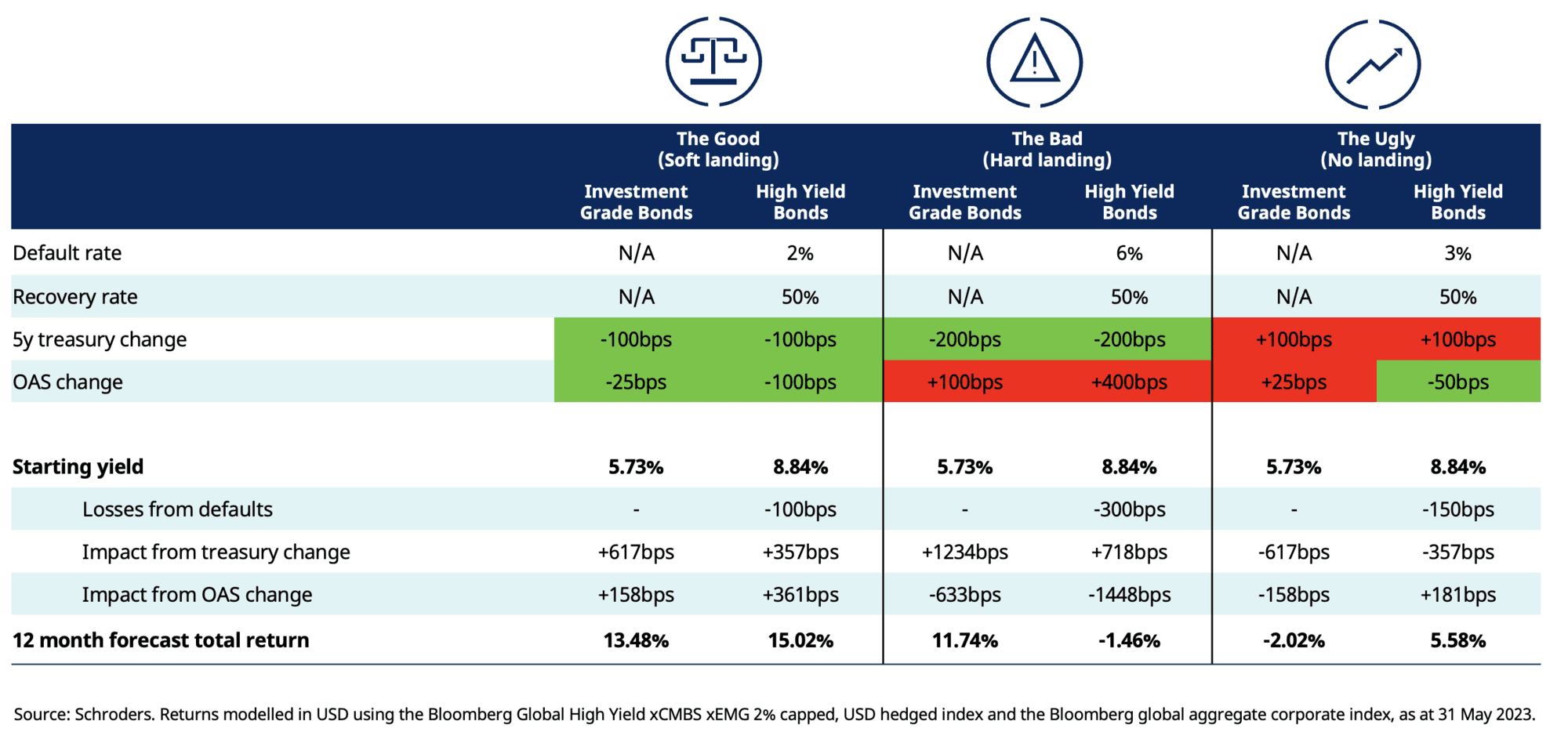

3. The Ugly – interest rates go back up

In this “no landing”—or perhaps more accurately “abortive landing”—scenario, inflation remains sticky and there’s a reacceleration of interest rate hikes. Corporate debt markets were pricing in an extreme version of the Ugly scenario for much of 2022 amid fears that quantitative tightening by central banks would jeopardise growth. We saw a milder version of this in February this year as signs emerged that inflation might be higher for longer, with the possibility that central banks might need to toughen their stance and potentially forcing a recession.

2. The Bad – hard landing

In this scenario, “the cure risks killing the patient.” A hard landing happens - a sharp fall in economic activity. You typically see rising unemployment, falling asset prices, pressure on banks, strained government finances and a general sense of economic instability. While central bank interest rate hikes get inflation under control, something in the economy breaks in this process. This scenario happened in March, with banks failing, starting with Silicon Valley Bank of the US collapsing. These bank failures happened because central bank tightening caused market yields to rise rapidly and eventually led to depositors withdrawing money en masse to take advantage of better returns elsewhere.

1. The Good – soft landing

In this scenario, economic growth slows, but to a sustainable rate without experiencing recession or a financial crisis, as well as managing inflation. Inflation has been tamed without too much damage to the economy. There’s no need for further interest rate rises and business conditions are healthy. This was the case at the beginning of 2023. Investment markets rose, as inflation expectations eased, and recession fears receded.

So, in the first three months of 2023 we saw a progression from Good, to Ugly, to Bad and then tentatively to Good again as it appeared that monetary and fiscal measures had successfully stemmed a wider banking crisis. It’s safe to assume we’ll see more oscillations in the next 12 months, so let’s put some numbers on what this might mean for asset allocation.

The table below looks at how the three interest rate and growth scenarios might play out on government bond yields and credit spreads (the yield premium for holding corporate bonds).

Note that this is not a real-world prediction or a recommendation, but a simplified illustration to give an idea of direction and scale of change.

Using the credit toolkit in different scenarios

The first thing to note from the table is how resilient credit can be as an investment. If we apply an equal probability to each scenario the 12-month forecast for total return is in excess of 6% in both investment grade and high yield. Investors can also protect themselves against any market falls by locking in an attractive yield at the offset.

Active security selection may also be able to improve on broad index outcomes by selecting bonds with more attractive yields.

Active bond selection allows investors to select the best instruments for the job in different environments. Credit investors face two main risks: interest rate exposure and credit exposure. The goal is to focus on the types of credit that can help capture the upside and reduce the downside risks. How might this work in practice?

Here are three most probable scenarios in the current environment.

1. The Good (interest rate risk falling, credit risk falling) - If you expect a soft landing, where rates are falling and business conditions are favourable, you’ll want to look for opportunities to add interest rate exposure with longer maturities and add credit exposure via high yield.

2. The Bad (interest rate risk falling, credit risk rising) - If you think rates have peaked but the economy is in trouble, you’ll want more interest rate exposure and less credit exposure, in other words, longer maturity bonds and more investment grade corporate debt. In this scenario default rates tend to rise, so this is where bottom-up research is most important. In fixed income investing, avoiding the blow-ups is more important than picking winners, and company-specific analysis is the best risk management tool to help do that.

3. The Ugly (interest rate risk rising, credit risk rising) - If you expect a scenario where interest rates bounce back up, the main priority is to reduce interest rate exposure, with short-dated or floating-rate credit. High yield corporate bonds are less interest rate sensitive because of their wider spreads (higher yield premium over government bonds), but it depends how ugly you expect the economic impact of the interest rate rises to be.

Implications for the 60:40 portfolio

Investors’ confidence in the value of the credit toolkit, and fixed income in general, took a hit last year as bonds failed to play their traditional role as a risk diversifier. But consider two data points: (1) this was the first year since 1969 that we’ve seen both bonds and equities fall and (2) the pace of US Federal Reserve rate rises was the fastest in 40 years. When markets are more worried about inflation than growth, bonds will struggle. But when growth concerns eclipse inflation concerns, that’s when the normal relationship is restored. We expect credit to come back as a good potential hedge for equities because of its versatile profile across different scenarios.

To read our latest credit insights and find out more about our funds, visit our website, contact your usual Schroders’ representative or call our Business Development Desk on 0207 658 3894.

Credit Market Scenarios

Important Information

Marketing material for professional clients only. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amount originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall. Schroders has expressed its own views and opinions in this document and these may change. This information is not an offer, solicitation or recommendation to buy or sell any financial instrument or to adopt any investment strategy. Nothing in this material should be construed as advice or a recommendation to buy or sell. Information herein is believed to be reliable but we do not warrant its completeness or accuracy. The material is not intended to provide, and should not be relied on for accounting, legal or tax advice. Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions. No responsibility can be accepted for error of fact or opinion. This document may contain “forward-looking” information, such as forecasts or projections. Please note that any such information is not a guarantee of any future performance and there is no assurance that any forecast or projection will be realised. Any reference to sectors/countries/stocks/securities are for illustrative purposes only and not a recommendation to buy or sell any financial instrument/securities or adopt any investment strategy. Schroders will be a data controller in respect of your personal data. For information on how Schroders might process your personal data, please view our Privacy Policy available at www.schroders.com/en/privacy-policy or on request should you not have access to this webpage. For your security, communications may be recorded or monitored. Issued in July 2023 by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority. UK0006481.