Jupiter Asset Management

Strong tailwinds

Harry Richards and Adam Darling, Jupiter Asset Management

Harry Richards and Adam Darling say investors have a once in a generation opportunity to lock in high yields in the investment grade corporate bond market.

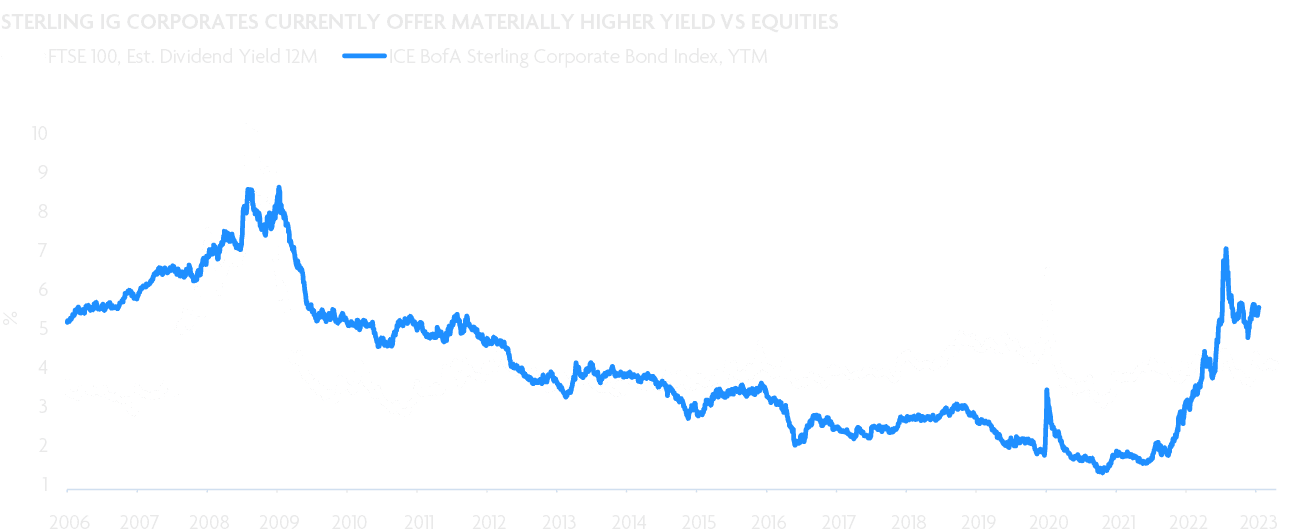

Investment grade bonds are now trading near the cheapest levels since the Global Financial Crisis, which provides a rare opportunity for investors to lock in high yields in a relatively safe part of the credit market as potential recession looms.

Major central banks including the US Federal Reserve (Fed), the European Central Bank and the Bank of England (BOE) have boosted their policy rates aggressively over the past year to induce a slowdown in growth and tame inflation. That effort is already bearing fruit, with inflation in the US as well as in the UK decelerating. That’s good news for investment grade bond investors, who can now look forward to much higher real returns, with market yields having trebled over the past two years. As growth falters, defaults at the lower rung of the credit spectrum may increase, further bolstering the appeal of high-grade bonds.

Long duration2022 and early 2023 saw one of the most extreme increases in government bond yields in modern history as the fear of sticky high inflation led central banks globally to embark on aggressive rate hiking cycles. Investment grade bonds suffered in this environment because of their relatively long duration, and hence higher exposure to interest rate volatility. The pain was even more pronounced in the Sterling high grade bond market.Investment grade companies typically tend to borrow for longer periods than those rated in the speculative category, as investors are more confident of getting their money back. However, longer duration bonds are more sensitive to changes in interest rates.

Improving prospectsAll that may be set to change for the better now as central banks are near the end of their monetary tightening spree as inflation has eased steadily from double-digit levels, and leading indicators of the economy suggest that inflation globally will continue to fall towards the 2% target. In this environment we think that longer duration assets, such as investment grade corporate bonds, could fare better both in terms of absolute and relative returns in comparison to other asset classes.

If we were to face a material recession across developed markets, inflation will likely fall even further, and interest rates could be cut aggressively.

This would be a positive scenario for high quality long duration assets as yields on government bonds would see a meaningful decline from current levels. Investment grade bonds, with low default risk and robust issuer characteristics, would be expected to materially outperform riskier asset classes into a weakening economic environment.

UK creditThe UK investment grade market looks particularly interesting at the moment. Credit spreads, the additional yield that investors demand to buy or hold investment grade corporate bonds compared to government bonds, are relatively cheap compared to long-run average/median spreads and look cheap relative to other investment grade markets globally (such as the US and Europe). This contrasts with tight spreads, for example, in the high yield market.

Recent volatility has created interesting tactical opportunities in sectors such real estate and financials. Real estate, in particular, is one of the sectors that suffered the most from the increase in interest rates. While fundamentals and certainly current news flow do not look bright for the sector as whole, in certain situations markets appears to have overreacted. Companies with high quality portfolios that are largely unencumbered, with modest leverage and low prevalence of floating rate debt can offer attractive value. In contrast, we are quite cautious on sectors with a higher degree of cyclicality such as consumer discretionary or industrials.

Across ratings, we see limited value in the A-rated segment of the market, while BBBs seem to offer more compelling risk/return prospects after their recent underperformance. Retaining some very high quality AAA and AA rated bonds in a portfolio helps to hedge against future volatility.

To be sure, as active managers we place a lot of emphasis on credit selection and try to avoid underperforming sectors and bonds of debt-laden firms that could be potentially downgraded. The crisis faced by Thames Water, Britain’s biggest water supplier, is a stark reminder of the importance of fundamental research. Even if there are no defaults, one needs to watch for credit spread volatility.

Overall, as we gear up for a recessionary world, we believe investors will flock to the relative safety of the investment grade market, with the attractive yield on offer a bonus. The market now offers an attractive entry point for locking in high yields, with the added advantage of boosting real returns as inflation softens. The shock of the drawdown in the bond market through 2022 means investors are a little cautious about their exposure to the asset class but that’s typically a good indicator of a favourable entry point.

Important Information

This document is intended for investment professionals and is not for the use or benefit of other persons, including retail investors. This document is for informational purposes only and is not investment advice. Market and exchange rate movements can cause the value of an investment to fall as well as rise, and you may get back less than originally invested. The views expressed are those of the individuals mentioned at the time of writing, are not necessarily those of Jupiter as a whole, and may be subject to change. This is particularly true during periods of rapidly changing market circumstances. Every effort is made to ensure the accuracy of the information, but no assurance or warranties are given. Holding examples are for illustrative purposes only and are not a recommendation to buy or sell. Issued in the UK by Jupiter Asset Management Limited (JAM), registered address: The Zig Zag Building, 70 Victoria Street, London, SW1E 6SQ is authorised and regulated by the Financial Conduct Authority. Issued in the EU by Jupiter Asset Management International S.A. (JAMI), registered address: 5, Rue Heienhaff, Senningerberg L-1736, Luxembourg which is authorised and regulated by the Commission de Surveillance du Secteur Financier. For investors in Hong Kong: Issued by Jupiter Asset Management (Hong Kong) Limited (JAM HK) and has not been reviewed by the Securities and Futures Commission. No part of this document may be reproduced in any manner without the prior permission of JAM/JAMI/JAM HK.